Days Sales Outstanding (DSO) in Asset Utilization Ratios

Several ratios measure the utilization or turnover of a company’s assets or liabilities. The most widely used is called the Receivables Collection Period or Days Sales Outstanding.

The Days Sales Outstanding (DSO) ratio is computed (in days) as follows:

Receivables Collection Period (Days Sales Outstanding) = Accounts Receivable / Credit Sales x 365

The collection period (DSO) can be compared to the company’s credit terms to get an indication of the quality of the receivables. If the for-credit sales figures are not available, a usable ratio can be made using total sales. If the proportion of credit sales to total sales remains stable over time, the trend may be analyzed even if the ratio is inaccurate. It will be consistently inaccurate, but the trend will correctly show whether collections are accelerating or stretching out. Note also that the number of days in the sales period must match the number of days in the calculation. If a quarter’s sales are used, 90 rather than 365 days should be in the calculation.

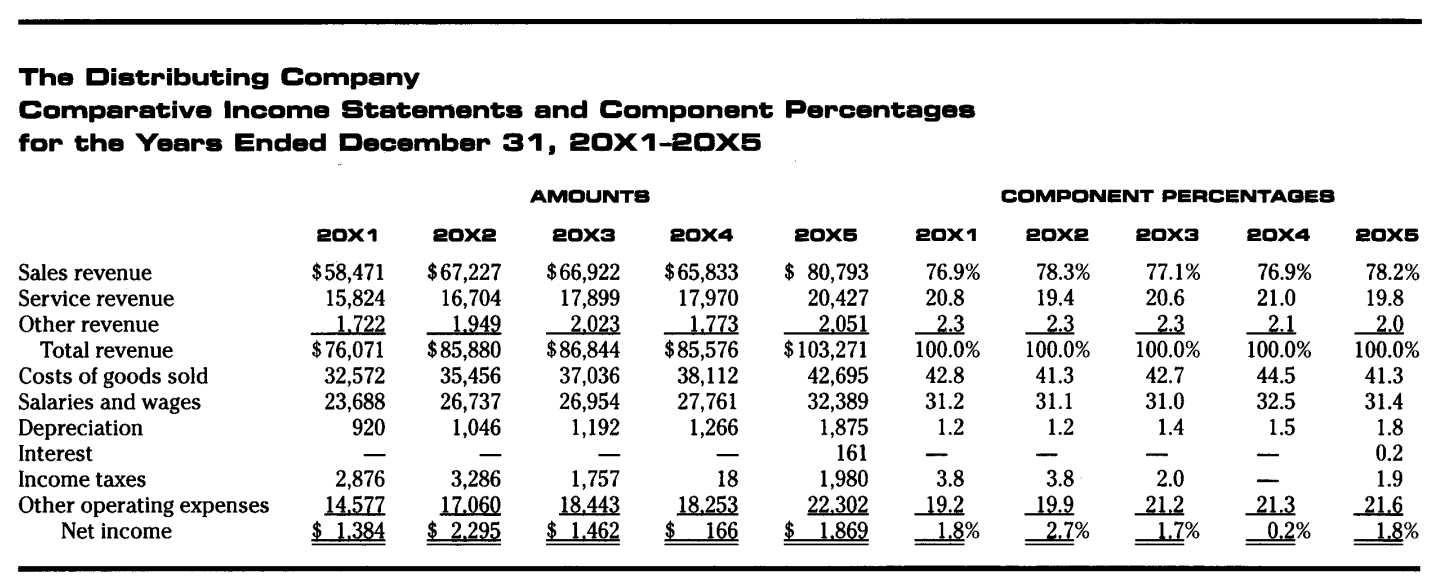

(The Distributing Company – Comparative Income Statements an Component Percentages for the Years Ended December 31, 20×1 – 20×5)

On total revenue, the collection periods for The Distributing Company in 20X4 and 20X5 were 11.2 days and 9.0 days respectively. Even based solely on sales revenues, the numbers are 14.5 and 11.6 days. These suggest the company probably has short credit terms and perhaps many cash transactions. Furthermore, although sales went up in 20X5, receivables dropped.

Another measure of asset turnover is Inventory Turnover, which is computed as follows:

Inventory Turnover = Cost of Goods Sold /(Inventory Beginning of Year = End of Years) / 2

This ratio expresses the number of times inventory was sold and replaced during a particular period. Again, no universal standard determines good or bad. Also, different methods of computing inventory cost (LIFO versus FIFO) distort comparisons among companies. The ratio can be useful, however, in identifying changes in the way a company is managing its inventory. The Distributing Company’s inventory turnover was 6.9 times in 20X5, a high figure reflecting its non-manufacturing nature.

It is sometimes possible to apply a measure to accounts payable similar to the collection period for accounts receivable. The Days Purchases Outstanding or Accounts Payable Period ratio is computed as follows:

Accounts payable period = (Accounts payable / Purchases) x 365

The result can be compared to credit terms extended by suppliers to see if the company is riding creditors or if accounts are paid promptly. The information needed to compute this ratio accurately may not be available to the outside analyst. The purchases figure is, however, often provided for smaller companies as part of deriving the closing inventory figure. For larger companies, the analyst must resort to using the cost of sales rather than purchases. This approximation usually will show a shorter payable period than the true period because non purchased items (such as labor and overhead) are included in cost of sales. Nevertheless, the trend in the payable period can suggest whether payment practices have changed.

A company with cash-flow problems will typically stretch its payable to gain a source of funds from its suppliers. This practice may be more expensive than negotiating a bank loan, but it can raise funds more quickly and with less explanation.

Note: The designation “Days Sales Outstanding” (DSO) is becoming more common, perhaps because “collection period” is a confusing term for what is actually the “non-collection” period. The term “collection period” also refers to a method of calculating the collection experience by determining the proportion of sales made in any given month that is collected in any subsequent month. For example, for sales made in any given month, the collection period may be 50 percent between 30 and 60 days later, 40 percent between 60 and 90 days, and 9 percent between 90 and 120 days with a 1 percent write off.

{kind=link}