Cost based pricing of Services | Problems | Methods used

Certain pricing structures are typically used to set the prices on services. They are Cost-based pricing, Competition-based pricing and Demand-based pricing. The following article explains the cost based pricing of services.

Table of Contents

Cost based pricing of Services

The basic formula for cost-based pricing is: Price = Direct costs + Overhead costs + Profit margin.

The service provider determines the price of the service by adding a percentage of profit to the costs. The service organization computes the cost of services by summing up material, labor and overhead expenses and adds a percentage of profit. It is also called cost-plus pricing.

Cost based pricing method is widely used by industries such as utilities, contracting, wholesale, advertising, building construction, engineering firms, consulting, etc. In case of professionals like consultants, psychologists, accountants, lawyers etc., ‘fee for service‘ is the pricing strategy used. This is based on the cost of time involved in providing service.

Special problems in cost-based pricing for services

1. Cost plus pricing is commonly used where component costs are calculated and a mark up added. This is quite easy in product pricing. But in service industries it is complicated because the tracking and identification of costs are difficult to arrive at.

2. It is very difficult to define the units in which a service is purchased. Many services are, therefore, sold in terms of input units rather than measured output. Most professional services such as consulting, engineering, architecture, psychotherapy and tutoring are sold in terms of hours.

3. Where multiple services are provided by the firm, it is difficult to calculate the costs in provision of service. For example, it is difficult for a bank to allocate teller time accurately across its checking, savings and other money transactions. So, difficulty arises in deciding the charges for the services.

4. With regard to services, employee time (rather than materials) forms the major item of cost, The value of time spent by people both professional and non-professional is difficult to arrive at.

5. Another inherent difficulty in most services is that the actual service costs do not adequately represent the value of the service to the customers.

6. Cost based pricing does not consider the price perception of the consumers.

7. In cost oriented pricing, it is essential to bifurcate costs into fixed and variable elements. But it is difficult to apportion fixed costs in case of multiple service offering.

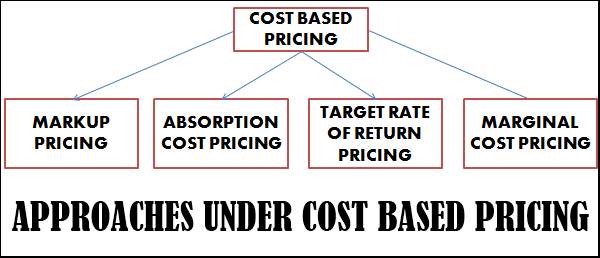

Various approaches or methods used in cost based pricing of services

The following image shows the various approaches or methods commonly used under cost based pricing.

1. Mark up pricing: Under mark up pricing, the selling price is fixed by adding a margin to the cost price of the product. Depending upon the nature of the service, product and market, the mark-ups may considerably vary. When the unit cost of the service is higher the mark-up is larger. Again when the turnaround of the service is slower, mark-up is larger.

Mark up pricing is based on the assumption that demand cannot be known accurately but costs are known. The objective of following mark up pricing is to maximize profits in the short and medium run. Generally, mark up pricing is followed by distributive trade and marketing firms who do not have any manufacturing unit of their own.

2. Absorption cost pricing: This is the full cost pricing method which is dependent upon the estimated unit cost of the service at the normal levels of production and sales. Under this method, various components of manufacturing such as variable costs, fixed costs, selling and administering the service are worked out. All these costs are added and required margin of profit is also included. This method does not consider demand factors by assuming the price to be a function of cost alone.

Absorption cost pricing method is not appropriate in a competitive market where the demand for the firm’s service product at the predetermined price cannot be taken for granted. The service provider, following absorption costing in a highly competitive market is sure to lose a considerable share of market.

3. Target rate of return pricing: The target rate of return pricing is similar to absorption cost pricing. Under absorption costing method, after the costs of manufacturing, the cost of administration and cost of selling are absorbed on a per unit basis, the firm adds the mark up towards profits. This mark up is arbitrary in nature. But under target rate of return pricing, a rational basis is used for arriving at the mark-up. The rate of return is linked to the level of production and sales assumed.

Such rational approach in pricing the service is followed by the general insurance companies such as New India Assurance company, National Insurance etc. They price their premium for car insurance according to the expected rate of claims and amount of.claims they may face from car owners.

4. Marginal Cost pricing: The aim of Marginal cost pricing is maximizing the contribution towards fixed cost. Marginal cost pricing realizes all the direct variables costs of services and a portion of the fixed cost. Though marginal costing is basically a cost-based method, it also considers demand aspects. So, marginal costing price is effective under competitive condition also. It is a flexible approach for realizing fixed costs through different service products. Marginal costing rests on classification of costs into fixed and variable components. In reality, there is also semi-variable costs. Such classification of costs is quite difficult in service industry. Where the fums are capital intensive, selling on marginal costs may not be appropriate.