Measures to curb Black Money in India

Table of Contents

Remedies or Measures to Curb Black Money in India

The menace of ever raising black money in Indian economy is very high. It is a well known fact that tax evasion generate black money.

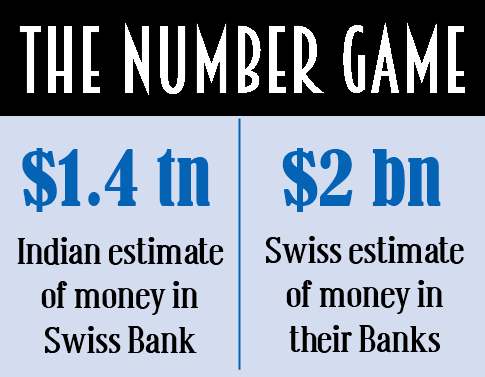

It is estimated that the volume of black money in 1991 has crossed over Rs. 1,00,000 crores. At present this is estimated to be about 1 trillion USD. Such staggering extent of black money has activated a parallel economy in the country and it affects the vital sectors of the economy.

The Government in the past has already tried certain measures with little success. If steps are not taken immediately to reduce the black money, it may ruin the entire economy of the country.

The important remedial measures for controlling black money are given below:

1. Demonetization

Demonetization of currency of high value say Rs.1,000 could help to unearth the black money to a large extent. However, in order to solve the problem arise on account of demonetization, proper step should be taken. It is advocated for eroding a substantial part of black liquidity on the presumption that black income held in cash will not be presented for conversion.

In 1978, Government cancelled currency note of Rs.1,000 denomination. But again it brought out the currency note of Rs.1,000 denomination for circulation. Demonetization may succeed in reducing the quantum of black money but it cannot prevent the generation of black money altogether.

2. Voluntary Disclosure Scheme

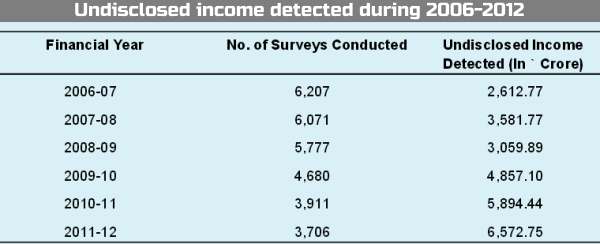

The Government may adopt the policy that those who voluntarily disclose their black income of the past to the taxation authorities will not be punished and penalties may be waived or minimized. The following image shows the amount of undisclosed income detected during the period 2006-2012. (Source: Whitepaper on Black Money, www.finmin.nic.in)

3. Raids

Income tax department’s powers have to be considerably enlarged and it should be empowered to conduct raids on the premises and properties of the taxpayers or any other individuals and can seize the unaccounted income and wealth and take necessary legal actions against the tax evaders.

4. Rationalization of Controls

Since ill-devised controls are major causes of black money, it is essential to rationalize the control system. Government has taken some steps in this direction by easing the licensing policy etc. But still there are many cumbersome rules and formalities and unnecessary control in many areas, which need to be effectively rationalized.

5. Taxation Reforms

India needs a rationalized tax structure. Prof. Kaldor, Wanchoo Committee and many others including the authors of the NIPFP Report have recommended a reduction in marginal tax rates, simplification of tax structure, taxation laws and improvements in tax administration.

6. Vigorous Prosecution

The Wanchoo Committee also recommended that the department should completely reorient itself to a more vigorous prosecution policy in order to instill a wholesome respect for the tax-laws in the minds of the taxpayers.

7. Special Bearer Bonds

In 1981 and 1991 the Government has introduced a scheme of Special Bearer Bonds to drag black money into the treasury’s coffer. It is advocated to unearth black money. But it is to be modified suitably according to the prevailing economic conditions.

8. Rewards and Awards

In order to encourage the honest taxpayers and create a positive attitude in the minds of the people towards the payment of tax, this can be adopted. The income tax department has introduced a special award scheme for the first time in Tamil Nadu for the 1994-95 assessment year, to encourage and recognize prompt tax payers and also create greater awareness in the minds of tax paying public.

It is called as “Good Taxpayers Award” Scheme. The various categories considered for the awarded scheme are: public and private sector companies, firms (both business and profession), individuals, and Hindu undivided families (both business and professions).

The other qualifications considered for the purpose of the award are that

- the person concerned should not only pay the highest tax but should also file the returns in time,

- prompt payment of taxes including self-assessment tax without default,

- no penalty for concealment of income should have been levied,

- no prosecution for offenses under the Direct Taxes Act and related provision of IPC should have been launched,

- no search undertaken under the Direct Tax laws should have been conducted, and should have been co-operative with the department in the completion of assessments.

Besides the above, no official patronage or recognition or awards should be given to persons who have been penalized for keeping the black money or in whose case prosecution proceedings have been taken.

9. Publicity

In view of the deterrent effect, the nature of all persons in whose cases penalties have been imposed for the concealment of income, wealth etc. should be published in the gazette as well as in the press, giving details of their names, addresses and the amount of penalties etc. If the assessee is a company or firm, the names of all the Directors of the Company or Partners of the firm should be published.

10. Arousing Public Conscience

A special drive should be undertaken to arouse public conscience by enhancing the co-operation of the leaders in various walks of life.

11. Other Measures:

- People should be educated with regard to real object of collections of taxes through press, radio, TV, and films.

- Steps should be taken to convince the taxpayers that the money collected through taxes is not spent wastefully but put to proper use.