Category of Revenues to Government | Tax Revenues

Table of Contents

Category of Revenues to Government

The revenues of the Government can be classified into two ways.

They are as follows:

- On the basis of mode of collection, and

- On the basis of nature of revenue.

1. Revenue on the Basis of Mode of Collection

It can be shown as follows:

1. Revenue on Compulsion: Taxes, Fines, Penalties, Forfeitures, Tributes and indemnities arising out of war or other, Compulsory Loans.

2. Revenue by Compulsory Payment: Income from Public property (Rent etc.), Income from, Enterprises, Fees, Licenses, Gifts etc.

3. Revenue Partly by Compulsory and Partly Voluntary: Special, Escheat, Printing of currency, Grants-in-aid etc.

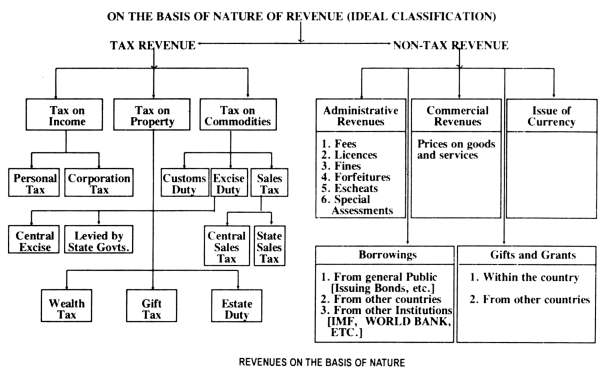

2. Revenues on the Basis of Nature

The revenues on the basis of nature can be classified as below.

Of these two, the revenues based on the nature are considered as the ideal classification. Let us explain these items one by one.

Tax Revenue of Government

1. Tax on Income

The Union Government imposes two types of taxes on income. They are as follows:

- Tax on personal income, and

- Tax on corporation profits.

1. Tax on personal income: The personal income tax is levied on the net income of individuals, HUF, firms and other association of persons.

2. Tax on Corporation Profits: The tax on the net profits of the joint stock companies is known as corporation tax.

2. Taxes on Property

The Union Government imposes different kinds of taxes on property. They are as below:

- Wealth Tax,

- Gift Tax, and

- Estate Duty.

1. Wealth Tax: Wealth Tax Act came into force on 1st April 1957. The wealth tax is charged every year in respect of net wealth of every individual, HUF and company at the rate specified by the Government.

2. Gift Tax: The Gift Tax Act came into force on 1st April 1988. The Gift Tax shall be charged for every assessment year in respect of the gifts made by a person during the year on the value of all taxable gifts.

3. Estate Duty: The Estate Duty Act came into force on 15th October 1953. It is levied on the principal value of all property, real or personal, settled or not settled which passes or deemed to pass on the death of a person.

3. Taxes on Commodities

The important taxes levied by the Union Government on commodities are:

- Customs Duty,

- Excise Duty,

- Sales Tax, and

- Service Tax.

1. Customs Duty: Duties on Import and Export of Goods constitute Customs duty. These type of duties are levied when the goods cross the boundaries of a nation. The Union Government levies it.

2. Exercise Duty: Excise duties are levied on the commodities produced in the country. It is levied both by the Central and State Governments. But it is levied according to the “Lists” given in the Constitution. Excise duties are now the major source of revenue to the Union Government.

3. Sales Tax: Both the Central and State Governments levy sales tax. The State Governments levy tax on the sales made within their respective jurisdiction whereas, the Union Government levies the central sale tax on the interstate trade or commerce.

4. Service Tax: Service tax is of recent origin. It was introduced by the former Union F.M of India Dr. Manmohan Singh in the year 1994-95. Initially, it covered the services of telephones, non-life insurance and stock brokers. But later its scope was extended to cover other services sector like advertising agencies, courier agencies, radio pager services etc. At present altogether it covers 96 types of services (Source). Now the effective service tax is 14.5% (as of 4th May 2016) including the Primary education cess 2%, Secondary and Higher Secondary Education Cess 1%.