Securitization | Definition | Stages | Merits | Benefits to banks

Table of Contents

What is Securitization?

“Securitization is a process by which financial institutions create additional liquidity on the backing of their existing assets through the sale of financial instruments”.

As business expands the need for various types for finance also increases. Financial institutions throughout the world are raising their resources, in the money market, capital market and debt instrument market. Governments are raising their finances by issuing various types of instruments. Thus, Securitization is a new concept by which financial institutions are able to acquire additional resources by using their existing long-term assets.

Example: Housing loan, vehicle loan, etc.

When banks and financial institutions provide long-term loans, the interest earned from them over a period. of time may decline due to the floating rate of interest. By way of Hedge, i.e., an insurance against the risk of declining interest rate, against these long-term assets, credit instruments are issued in the market for a lesser rate of interest and additional funds are added. The funds raised by the sale of the debt instruments such as CD (Certificate of Deposits) will be utilized for providing short-term or medium-term loans.

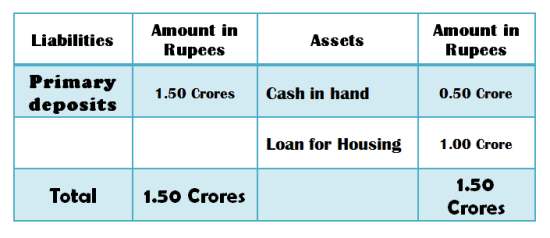

We can explain securitization in the following balance sheet of a bank.

Now the bank can transfer the housing loan to a Trust and obtain from them Rs. 1 crore worth of funds against which it can issue Certificate of Deposits carrying lesser rate of interest than the housing loan.

For example, the housing loan may carry 10% interest while the Certificate of Deposit may carry only 8%. Even if the housing loan interest falls due to floating rate of interest, it will not affect the bank due to Hedge.

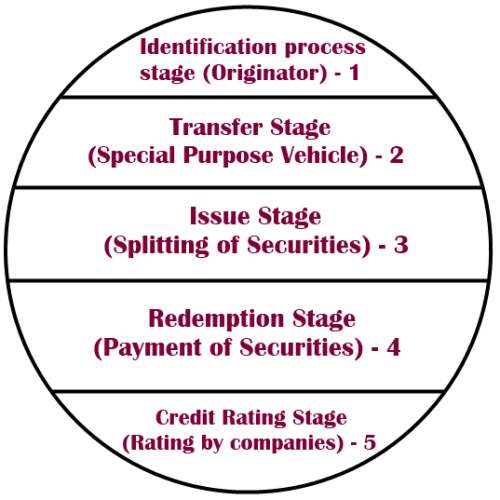

Stages involved in Securitization process:

First stage in Securitization:

In the first stage, the financial institution or the banker, is called the ORIGINATOR. The ORIGINATOR will pool his lending like mortgages, or account receivables into a homogeneous type based on interest rate, maturity period, etc. Thus, the first stage is called Identification process stage.

Second stage in Securitization:

The originator will transfer all his assets to another institution which helps in the process of securitization. The assets are converted into securities by SPECIAL PURPOSE VEHICLE (S.P.V) or Trust. The Trustees may be retired high court judges who may have knowledge of valuation of assets and finance. There are also merchant bankers who act as SPV and as agents for issue. The reputation of merchant bankers will help in the issue of debt instruments by which the debt instruments will be oversubscribed.

Issue stage in Securitization:

The SPV splits various assets into different types of securities according to their maturity date and interest rate.

The SPV issues securities to investors which are as follows:

- Pass through certificates

- Pay through certificates

- Interest only certificates

- Principal only certificates

Pass through certificates:

In the case of Pass through certificates, payments are received from assets such as housing loan from out of which payment for certificate of deposits are met as and when they are due.

Pay Through certificates:

In this case, multiple maturity structure certificates depending upon maturing pattern of various assets will be issued, so that as and when the assets mature the respective certificates will be paid.

Interest only certificates:

The interest for these certificates will be paid as per the earnings from the assets securitised.

Principal only certificates:

Only the principal amount will be paid on the certificates from the realization of assets.

Redemption stage in Securitization:

Payments received from various assets are used for redeeming various credit instruments issued. This is done by the originator himself. In some cases, a separate servicing agent may be appointed who will undertake collection work for which adequate commission will be paid. The job of the servicing agent will be to discharge the assets through the collection of principal and interest and settle the debt instruments.

For example, the housing loan may be collected with principal and interest and fi.om its collection, debt instruments such as certificate of deposits will be met.

A pass through certificate which we have mentioned already may be a with recourse or without recourse certificate. In the case of with recourse certificate, if payment is defaulted, the originator will be held liable by the SPV. Hence, SPV plays a major role in settling the claims of the investors.

Credit rating stage in Securitization:

The pass through certificate issued by SPV has to be credit rated as they are debt instruments which are issued to the public. The financial institutions issuing these debt instruments will have to undergo credit rating which is statutorily mandated in certain countries. The debt instruments are also traded in the secondary market especially for interest swap.

The following are the various assets which can be used for Securitization by financial institutions.

- Housing loan granted to individuals or institutions

- Hypothecation of vehicle loan

- Leasing finance, especially financial lease

- Supply bills belonging to government departments

- Outstanding on credit cards

- Long-term loans granted to reputed parties.

Diagrammatic Representation of Stages involved in Securitization Process:

The stages discussed above can be diagrammatically represented as follows:

Merits of Securitization

- It enables the lending institutions to improve their liquidity by converting their long-term assets for Securitization.

- With increasing turn over of the raised liquidity, the earnings of the originator goes up.

- Financial institutions can gain in Securitization by interest swap

- As the assets structure and volume are reduced, the capital adequacy ratio is increased and it reduces risk on the assets.

- From the long-term assets, funds are raised and invested in various debt instruments which brings diversification of risks.

- The financial institution is able to get a better credit rating and this enables them to obtain funds at lower cost.

- Mutual funds and other financial institutions such as insurance companies will be benefited due to different portfolio investments.

- Increasing demand in the money market can be met from out of the long term assets and this will make the capital market more dynamic.

Benefits of Securitization to banks:

Commercial banks have an important responsibility of protecting the interests of depositors and at the same time provide them with attractive interest rates. This balancing act can be done only when commercial banks undertake Securitization. Precisely, the commercial banks enjoy the following benefits due to Securitization.

- They obtain better source of funds.

- They are able to maintain capital adequacy norms wherein high risks assets are countered by lower risks weighted assets.

- Banks can create more credit since they can shift from one portfolio of investment to other, especially during selective credit control.

- By interest swap and by turn over, the earnings of the banks increases by which profitability goes up.

- Benefits to Assets Liability Management: When there is floating rate of interest, the income of the bank may be affected. This may be countered by the bank switching over to higher interest earnings so that its income will be sufficient to meet the claims of depositors.