How are profitability measured?

Profitability is measured in two ways

- Profits related to revenue and

- Profits related to investment.

Table of Contents

Profitability relative to revenue:

The gross measure of profitability on revenue is the ratio of net income to sales:

Return on Sales = (Net Income / Sales)

When this relationship is stable, it can be used to forecast future profits once an estimate of future sales has been made. In most cases, however, the relationship varies because of changes in prices, product mix, and expense components. Thus, a detailed review of the relationships among the expense components of the income statement and sales is useful.

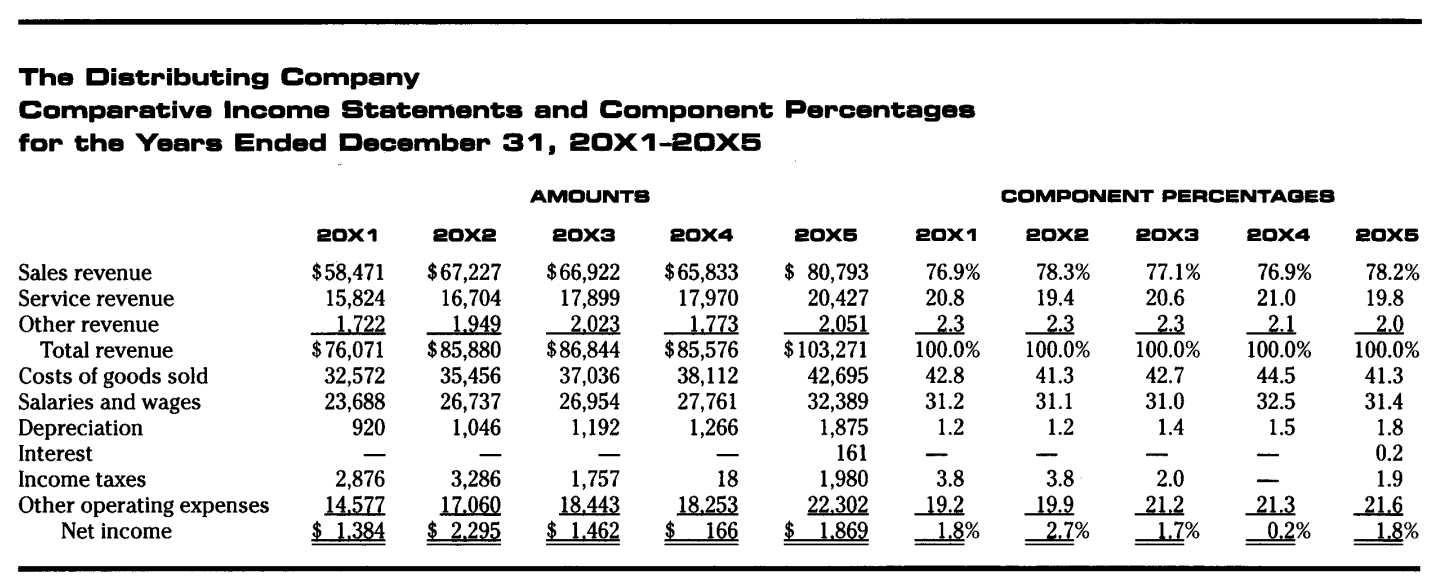

A typical component-percentage income statement is provided below. Revenue is usually the key item in an income statement, and the level of many expense items is related directly to the volume or revenue. In The Distributing Company, the cost of goods sold is the largest single expense. It has varied between 41.3 percent and 44.5 percent of total revenue. After the cost of sales peaked in 20X4, management apparently brought the costs under control in 20X5.

For most companies, changes in gross margin and net profit percentages are important items for analysis. Different ratios would apply to a service operation, such as a taxi company. For the taxi company, salaries and wages, fuel, and maintenance expenses might be the most important items for analysis.

Profitability relative to assets employed:

The continuation of a business hinges on its ability to earn a satisfactory return on the assets employed. Failure to do so may severely limit the firm’s access to funds for growth or even for maintenance. A measure of this return is often computed as follows:

Return on Assets = Net Income / Assets

(The Distributing company – Comparative Income Statement and Component percentages for the years ended December 31m 20×1-20×5)

From the above image, the Return on Assets (ROA) for The Distributing Company for 20X5 is calculated as follows:

Return on Assets = $1,869 / ($11,058 + $10,959) / 2 = 16.9%

There are several variations used in computing the Return on asset ratio. These include adjustments for interest expenses, non-operating assets, and other items that affect the operating income and operating assets. One alternative, for example, measures the earning power of the assets without the distortion created by the amount of debt in the capital structure and by changing tax rates. This ratio, which uses the earnings before interest and taxes (EBIT) in the numerator, is computed as shown below. This measure can be termed the Before Tax Return on Unlevered Assets (a variant of the return on assets calculation).

Return Before Taxes on Unlevered Assets = (Earnings Before Interest and Taxes / Average Total Assets)

For small businesses in particular, a company’s cash-flow-generating capacity is more important than income measures. The ratios described above can easily be changed to substitute a measure of cash flow in the numerator. For instance, earnings before interest and taxes (EBIT) may be replaced with earnings before interest, taxes, depreciation, and amortization (EBITDA).

These ratios must be interpreted by considering the dollar costs ascribed to the assets and how net income (or cash flow) is calculated. For example, a company with older plant and equipment, purchased when the dollar was less inflated and largely depreciated, may show a higher ROA than a company with newer assets and a higher gross margin. The asset investment of the first company is so small its ROA overwhelms the more efficient performance of the second. The ratio calculated using the EBITDA figure may show the reverse, however. Also, companies with the same assets can report significantly different income depending on the accounting principles they use for such items as depreciation and inventory.

This ratio measures earning power from the viewpoint of the equity investor — after payment of interest and taxes. The Return on Equity (ROE) is typically computed as follows:

Return on Equity = (Net Income Available for Shareholders / Shareholders’ Equity)

This measure appropriately uses net income; all claims above the common stockholders’ claim on the company’s earning have been deducted. If the firm has preferred stock outstanding, the dividends on this form of equity are subtracted from the net income for shareholders to derive the net income available for common shareholders. A Return on Common Shareholders’ Equity can be calculated by using the adjusted net income in the numerator and the common shareholders’ equity in the denominator.

Note: Typical of the confusing nomenclature in the finance area is the term Return on Investment (ROI). Whether it refers to the ROA or the ROE can only be determined by inspection. The ROI can also refer to a measure of return on total capital, such as EBIT Capitalization.

A further variation, for companies with publicly traded equity, is to calculate the ROE measures using the market Value of the equity in the denominator. This ratio is called Return on Equity Market Capitalization. A similar return ratio can be calculated using all of the securities in the company’s capital structure at their market value. This ratio is called Return on Total Market Capitalization.

It is very common to use the book value of the debt, however, in computing this ratio rather than to obtain market values. First, a market value for most debt is not available because the debt is not traded. Thus, an effort must be made to estimate the value of the debt by extrapolation from value of traded debt of the same risk rating. Second, most corporate debt now has a floating interest rate. The presumption therefore is that the debt would trade close to its book value.

{kind=link}